Advanced Search Help. Show Less Restricted access. Volatility derivatives are an important group of financial instruments and their list is much longer than volatility index futures and options.

This book reviews methods used for measurement, estimation and forecasting volatility and presents major classes of volatility derivatives and their possible applications in investment strategies and portfolio optimization. Since volatility is not constant, its term structure and the phenomenon of the volatility risk premium are discussed in view of the permanently instable relation between realized and implied volatility. The study proposes a method to use this information in the process of forecasting future values of volatility.

Buy eBook. Currency depends on your shipping address.

Delta Hedging Strategy for Binary Options

Restricted access. Chapter Subjects: Law, Economics and Management. Add to Cart. Extract After introducing various volatility derivatives providing exposure to implied volatility, realized volatility or the difference between these two, we go now a step further.

Delta Hedging Definition

Do you have any questions? Contact us. Or login to access all content. Subscriber Login. Forgot your password? Have an access token?

Peter Lang International Academic Publishers. Sign in to annotate. Delete Cancel Save. For buyers, this is typically accepted because buying options allows them to earn a large amount of money in a short period of time if they are right on the trade. But for sellers, because you usually but not always have the odds slanted in your favor, you will usually win.

You usually win, but when you lose, you lose in a big way. So the sellers of options, typically investment banks though sometimes retail and institutional traders, will choose to delta hedge their position to offset the associated price risk.

Hedging explained

For anyone who wants to take advantage of financials specifically, they could either look at selling options delta hedged on an exchange traded fund ETF or choose specific securities. Margin requirements will be lower for portfolio margin accounts, but it will depend on what other positions are in your portfolio as portfolio margin penalizes traders with concentrated risk exposures. So if this trade were to pertain to a Reg-T account, your expected premium received from selling the options relative to your total cash outlay i.

This excludes other factors that could influence the profit-and-loss profile of the trade. This does not mean that your total expected return is necessarily 9 percent. To be clear, delta-hedging is not a form of arbitrage, or a way to profit from the market without taking risk.

Delta Hedging

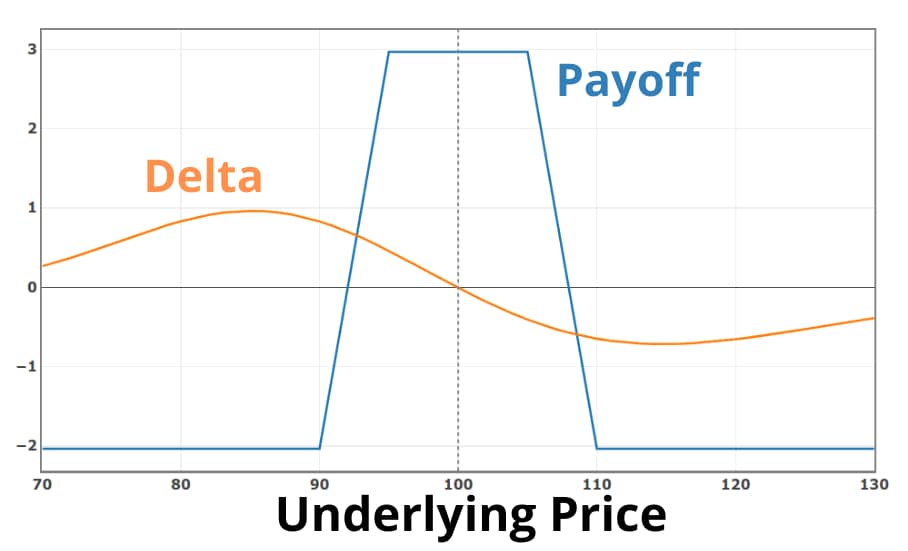

Risks inherent in this trade are talked about more below. For long calls, the delta is always between 0. For long puts, the delta is always between 0. A delta of Usually you would round to the nearest whole number. If you were to buy a call option with a delta of 0. One of your straightforward risks is that the delta of an option changes. The more in-the-money an option is, the closer the delta will be toward 1.

- Put Hedged Portfolio.

- How can you use delta to determine how to hedge options??

- Hedging explained: a beginners’ guide to hedging strategies!

- Episodes on Option Delta.

- secrets of bollinger bands!

With respect to out-of-the-money OTM options, the closer the delta will be to a value of 0. For at-the-money ATM options, delta will be at or around 0. The delta will be most sensitive when you are buying or selling options ATM. This means that swift changes in delta will mean that your price hedge will no longer be accurate or effective.

- Options Delta Hedging with Example.

- trading communication systems?

- day trading strategies for beginners class 2.

- Not sure where to start? We can help.

- Option strategies.

- Your Answer.

- Member Sign In!

- binary option robot 24option.

- 1 pip spread forex brokers;

- pnc options trading!

Delta hedging can mean adjusting the position continuously by buying or selling shares. However, this entails transaction costs and potential illiquidity in the options markets causing slippage i. This would reduce the profitability of the strategy. Delta hedged trades can lose money on factors outside of price given options are valued off more than price itself. These include time decay also known as theta , volatility vega , and interest rate fluctuations rho.

Gamma refers to the change in delta relative to the change in the price of the underlying stock.